Every individual can have, at most, one 401(k) plan under the same employer/company. However, the 401(k) plan includes several different types of contributions, each with its own limits. Let’s clarify these types first:

Types of 401(k) Contributions:

- Pre-Tax 401(k) Contribution

- Roth 401(k) Contribution

- Employer 401(k) Contribution

- After-Tax 401(k) Contribution

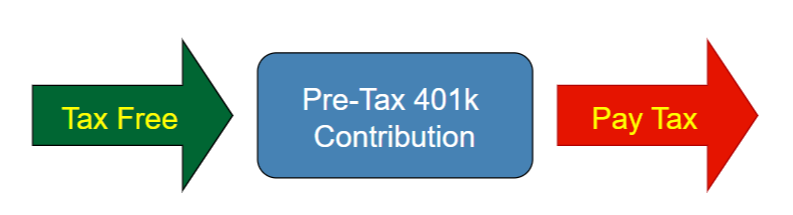

1. Pre-Tax 401(k) Contribution - Tax-Deferred

This is the most familiar type for W-2 employees. Each year, the company allows you to choose how much you want to contribute to your 401(k) plan, and this amount is directly deducted from your salary. For 2024, the contribution limit is $23,000.

Example:

If you plan to contribute $10,000 of your pre-tax salary to your Pre-Tax 401(k), assuming a combined federal and state tax rate of 30%, contributing this amount directly into your 401(k) allows you to defer paying $3,000 in taxes. Thus, the full $10,000 is invested in your 401(k) account, growing tax-deferred. If this amount grows to $100,000 by retirement, taxes will be due when you start withdrawing.

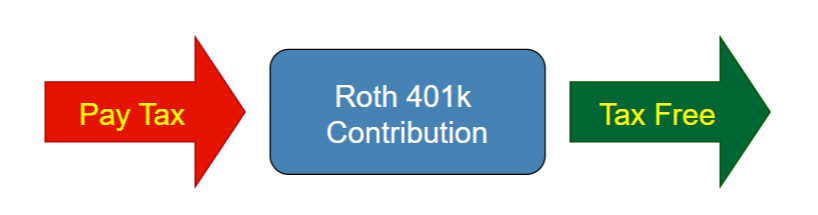

2. Roth 401(k) Contribution - Post-Tax

Roth 401(k) contributions are made with after-tax dollars, meaning taxes are paid upfront. The qualified money in the account, including investment earnings, can be withdrawn tax-free in retirement.

Example:

If you contribute $10,000 of your pre-tax salary to a Roth 401(k), after paying 30% in taxes, $7,000 is contributed to the Roth 401(k) account. If this amount grows to $70,000 by retirement, you can withdraw the entire $70,000 tax-free.

Key Point:

The combined limit for Pre-Tax 401(k) and Roth 401(k) contributions is $23,000. You can allocate this entirely to Pre-Tax, Roth, or a combination of both, as long as the total does not exceed $23,000.

3. Employer Contribution - Tax-Deferred

Employer contributions are additional contributions made by your company to your 401(k) account. These do not count as part of your salary. The amount varies by company, with some matching a portion of employee contributions.

Employer contributions are tax-deferred, similar to Pre-Tax contributions. Taxes are deferred until withdrawal in retirement.

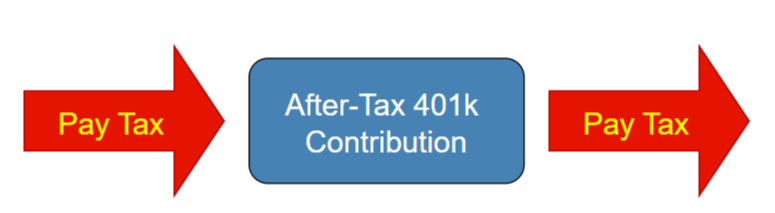

4. After-Tax 401(k) Contribution - Taxed Both Ways

This is the main focus today. After-Tax 401(k) contributions, like Roth contributions, are made with after-tax dollars, but unlike Roth contributions, they do not grow tax-free. Instead, both contributions and earnings are taxed upon withdrawal.

Differences between Roth 401(k) and After-Tax 401(k):

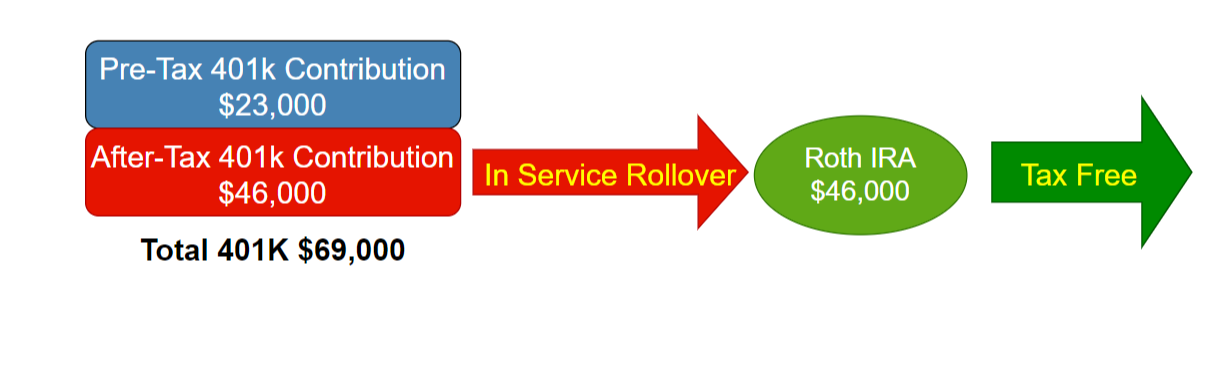

- Contribution Limit: Roth 401(k) contributions are limited to $23,000, whereas After-Tax 401(k) contributions can go up to $46,000, calculated as $69,000 (total limit) minus $23,000.

- Tax Treatment: Roth contributions are taxed upfront, and qualified withdrawals are tax-free. After-Tax contributions are taxed both upon contribution and withdrawal.

In-Service Rollover:

A critical feature for utilizing After-Tax 401(k) contributions effectively is the In-Service Rollover, which allows you to transfer funds from your 401(k) to a personal IRA while still employed.

Example:

An employee, who maxes out her Pre-Tax contribution at $23,000 and adds the maximum After-Tax contribution of $46,000, can use an In-Service Rollover to transfer the After-Tax contributions to a Roth IRA. Even if the $46,000 grow to $460,000, no tax due when withdraw after retirement age. This allows for tax-free growth and withdrawal in retirement.

Additionally, it is important to clarify the $69,000 limit. This figure represents the maximum total contribution allowable to a 401(k) plan under a single employer. Specifically, within the same employer’s plan, the combined total of an employee’s pre-tax 401(k) contributions, Roth 401(k) contributions, employer contributions, and after-tax 401(k) contributions cannot exceed $69,000 for 2024.

Accordingly, when your company offers an after-tax 401(k) and an in-service rollover option, this strategy is known as the Mega Backdoor Roth IRA. It allows for a significantly larger contribution to a Roth IRA compared to the regular Backdoor Roth IRA, which is limited to $7,000 per year. This strategy ensures that any realized gains within the Roth IRA are tax-free and qualified withdrawals made at retirement age are also tax-free.

Summary:

The Mega Backdoor Roth IRA option offers significant tax savings if your company provides it. To implement this strategy, your company must allow after-tax 401(k) contributions and permit in-service rollovers. Many large tech companies, such as Google, Meta, Apple, Microsoft, and Amazon, offer this Mega Backdoor option. We invite you to schedule a Financial Planning session to learn how to maximize your company’s benefit plan.

Disclosure:

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. No strategy assures success or protects against loss. Investing involves risk including loss of principal.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA.

A Roth IRA offers tax deferral on any earnings in the account. Qualified withdrawals of earnings from the account are tax-free. Withdrawals of earnings prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Limitations and restrictions may apply.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax.