The WA Cares Fund is the nation’s first state-mandated, publicly funded long-term care (LTC) insurance program. Although it has been collecting payroll taxes for just over a year, its future may be at risk while other states explore their own LTC solutions.

With the new year came new state legislative sessions. Bills from previous sessions that showed promise but failed had to be reintroduced. Legislative activity has been less intense compared to 2023, as “even years” often see shorter sessions due to elections. Nonetheless, there are still some important updates.

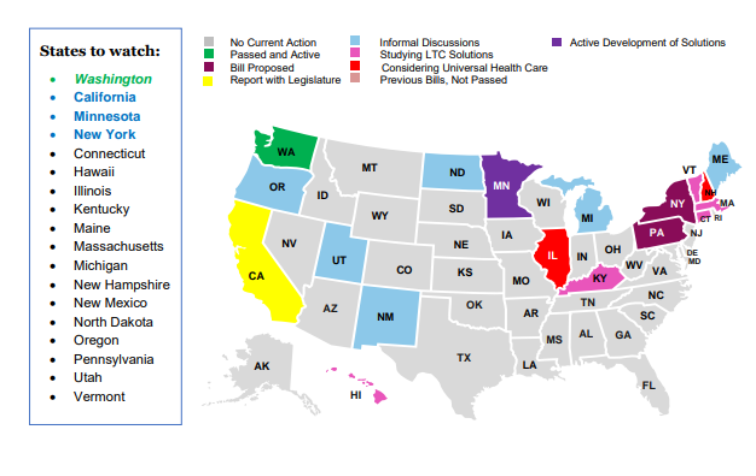

Here is the list of states to watch: Source from Nationwide Retirement Institute

California

In 2023, the California LTC Task Force proposed options for a potential program and Oliver Wyman Consultants delivered a report of the final five options on December 18, 2023. However, the deadline to propose new bills to the CA legislature in 2024 has passed (February 16, 2024), and the Task Force was officially dissolved on July 1, 2024.

This delay may provide legislators more time to review the Oliver Wyman report. It remains unclear what type of LTC coverage might qualify if a bill is proposed in 2025, including whether inflation adjustments or minimum benefit amounts will be required.

When legislators eventually consider the Oliver Wyman Report’s options, it is hoped they will adopt the reduced tax option for employees with qualifying LTC insurance after any opt-out deadline. This would help maintain tax revenue while minimizing the risk of California needing to pay benefits, as private policies would need to be exhausted first.

Washington

Washington state is back in focus, not just for potential improvements to its existing program but because of Initiative 2124. The group “Let’s Go Washington” has gathered the necessary signatures to place this measure on the November 2024 ballot.

Authored by State Rep. Jim Walsh (R-19), the “Opt Out of State-Run Long Term Care Coverage Act” would make participation in the WA Cares Fund optional. If passed, it would allow anyone in the program to opt out, potentially jeopardizing the program’s solvency or even leading to its collapse if enough people opt out.

- Opt-out:

The private insurance exemption has expired. To qualify for the opt-out, residents needed to purchase an LTC policy before November 1, 2021, and apply for their exemption with the Employment Security Department (ESD) by December 31, 2022. Simply owning a qualifying policy during this period is not sufficient; the exemption certificate had to be obtained by the deadline. Moving to Washington after this date does not alter these requirements.

- Who can opt-out currently:

- Reside outside Washington while working in the state

- Be a spouse or registered domestic partner of active-duty U.S. military

- Be a veteran with a 70% or higher service-connected disability (permanent exemption)

- Hold a non-immigrant work visa; if a Green Card is later obtained, it must be reported to ESD, and the employee will be enrolled in the program

To qualify for these exemptions, employees must apply for an exemption certificate with ESD and provide the certificate to their employer.

Minnesota

Minnesota has been exploring various solutions for LTC funding. Recently, the state commissioned a study to recommend changes to Long-Term Services and Supports (LTSS) and identify funding options. The recommendations include:

- Care Navigation & Support Services: A state-run program to enhance care for older adults through existing services, education, and support for families and caregivers. This initiative aims to promote Home and Community-Based Services (HCBS).

- Medicare Companion Product: A new insurance product to coordinate care needs in retirement, offering two options:

- Voluntary Market Option

- Compulsory Option: Provides $135 per day for one year, costing about $120 monthly at age 65, with premiums and benefits increasing 3% annually.

- Catastrophic-Lite State Program: A mandatory state insurance program covering long-term care expenses for up to five years, after a two-year waiting period. It focuses on HCBS but also covers facility care. The program would be funded through payroll taxes.

- Benefits: Up to $50,000 annually, $250,000 over five years, with 3% annual inflation.

- Estimated Cost: 0.55% to 1.15% in payroll taxes.

The first option is the easiest to implement, but all three options may be considered over time.

New York

New York introduced two LTC bills in 2024: Senate Bill 8462 on January 31 and Assembly Bill A10143 on May 10. Neither bill will pass this year due to the end of the legislative session.

Senate Bill 8462, updated from the 2022 version, now includes self-employed individuals and adds four permanent exemptions:

- Veterans with a 70% or higher service-connected disability

- Individuals with non-immigrant work visas

- Employees living outside New York

- Spouses or registered domestic partners of active-duty military

The bill also adjusts vesting for those born before January 1, 1972, to receive benefits based on years worked and changes eligibility from 3 out of 10 ADLs to 2 ADLs, excluding cognitive impairment.

No changes have been made to the LTC policy qualifications for opt-out, which still apply only to traditional LTC insurance. The New York legislature is out of session for the rest of the year due to budget constraints, but new bills may be proposed in future sessions.

Maryland:A bill to study LTC solutions was proposed earlier this year but both sponsors withdrew it. No current action is taking place in Maryland.

Pennsylvania: A bill similar to the WA Cares Fund was proposed again in 2023 (H 844), including a 0.58% premium tax and an LTC insurance tax exemption. The two-year session ends on November 30, 2024, with no current movement or committees formed. Future attempts may be made.

Illinois and New Hampshire: Both states previously proposed universal health care programs with LTC coverage, but details are unclear. Concerns exist that these programs might ban the sale of LTC insurance within the states, limiting options for residents. Future developments will be monitored.

The importance of having private LTC coverage

Choosing to opt out of a state-mandated LTC program is a personal decision. However, having private LTC insurance—regardless of state programs—is beneficial for several reasons:

- Custom Coverage: Private policies offer benefits tailored to your preferences, including full cash indemnity, unlike state programs which often limit payments to approved providers or reduced cash payments.

- Guaranteed Terms: Private insurance provides guaranteed premiums and benefits, whereas state programs may increase tax rate or reduce benefits to stay financially viable.

- Better Benefits for High Earners: Private insurance offers better leverage for high earners. State programs might tax them more than the benefits they provide.

- Broader Care Options: Private insurance allows for more flexible care choices. State programs may restrict options to approved providers and require certifications for family caregivers.

- Portability: Private insurance is generally portable between states and sometimes internationally. State programs may restrict out-of-state benefits.

- Inflation Protection: Private policies can include guaranteed annual inflation adjustments, which state programs may not offer.

- Premium Protection: Some private policies linked to life insurance or annuities offer premium protection. State programs do not refund unused benefits or premiums.

- Timely Planning: Plan ahead to avoid last-minute opt-out deadlines and to secure better rates and coverage before potential health declines.

- Increased Marketability: Private insurance is valued by care providers, who prefer patients with coverage that pays the billed rate, unlike state programs that may only reimburse at Medicaid rates, which might not cover the full cost of care.

Summary

State LTC programs can assist many people, but those who can afford private LTC insurance might find additional value in the flexibility and benefits it offers. Private coverage often provides more choices for care and can be portable across states and internationally. Ideally, states and legislators will recognize the private LTC industry as a valuable partner and seek collaborations that benefit everyone.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. Fixed annuities are long-term investment vehicles designed for retirement purposes. Gains from tax-deferred investments are taxable as ordinary income upon withdrawal. Withdrawals made prior to age 59 ½ are subject to a 10% IRS penalty tax and surrender charges may apply. A long term care rider is an additional guarantee option that is available to an annuity or life insurance contract holder. While some riders are part of an existing contract, many others may carry additional fees, charges and restrictions, and the policy holder should review their contract carefully before purchasing. All guarantees are based on the claims paying ability of the issuing insurance company.