As you consider your long-term care (LTC) insurance options, it's important to note the evolving landscape of state-mandated programs. The WA Cares Fund, a pioneering program in Washington, is a significant development in this area. Despite initial delays, it's now operational, and other states are observing closely, debating whether to implement similar programs or take a different approach.

At the start of the new legislative year, states are reassessing past bills and introducing new ones. While not all states are immediately considering a tax-based solution, about 30% show interest in addressing LTC challenges. This means the situation is fluid, and keeping informed about these developments is key to making educated decisions about your LTC coverage. Understanding these trends will help you navigate your options and plan effectively for your future care needs.

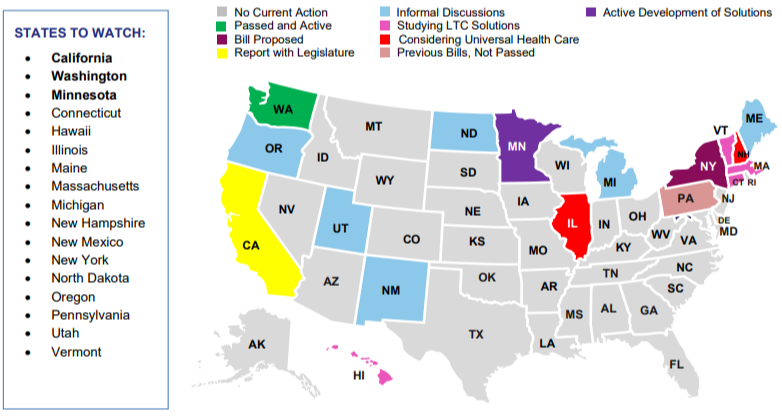

California

As you consider your long-term care (LTC) insurance options in California, it's essential to be aware of the recent developments. The California Task Force, in collaboration with Oliver Wyman Consultants, has conducted extensive work in proposing options for a state LTC program. Their report, detailing alternative features and pricing for the top five options, has been submitted to the California legislature.

Despite this progress, it seems unlikely that a bill will be proposed in 2024, since the deadline for new bill proposals (February 16th, 2024) has already passed. This delay could be advantageous, as it gives legislators more time to delve into the report, ask questions, and gain a comprehensive understanding of the options before drafting legislation.

Looking ahead to 2025, questions remain about the criteria for LTC coverage to qualify for any opt-out or reduced tax options. Details such as the requirement for inflation protection, minimum benefit amounts, and the nature of qualifying policies are still uncertain.

The Oliver Wyman report suggests a public/private partnership model, where private LTC policyholders might receive tax benefits. This model encourages the purchase of private LTC insurance by offering back-end benefits after private coverage is exhausted, a proposal yet to be adopted.

As of now, no study group has been formed to define the structure of LTC policies for opt-out or reduced tax eligibility. There's also no established deadline for purchasing policies that would qualify under these potential rules.

Washington

Yes, Washington state has reemerged on the radar, and it's not merely to monitor ongoing program enhancements. A group named “Let’s Go Washington” seems to have secured the necessary signatures to include Initiative 2124 on the November 2024 ballot.

The "Opt Out of State-Run Long Term Care Coverage Act," authored by State Rep. Jim Walsh (R-19), is at the forefront of this initiative. If Initiative 2124 were to pass, it would revolutionize the program by allowing optional participation and permitting current members to opt out for any reason. Such a change could potentially undermine the program's solvency without further adjustments, or, if a significant number opt out, it could jeopardize the funding of the WA Cares Fund. While the Washington legislature has the option to propose an alternative alongside the initiative, they have yet to do so.

If Initiative 2124 is successful, individuals who bought LTC coverage solely to opt out of the tax might reconsider their decision.

Minnesota

This state has been intriguing to observe as it has diligently explored various potential solutions over the years. Recently, Minnesota commissioned a study to gather recommendations for restructuring LTSS and to identify potential funding options.

The recommendations resulting from the stakeholder process include the following proposals:

- Care Navigation & Support Services

- Establishment of a state-initiated and collaborative care navigation and support service for all older adults, aimed at leveraging existing services, enhancing awareness and education, and providing assistance to families and informal caregivers throughout their care journeys via online and telephonic means. The initiative seeks to promote Home and Community Based Services (HCBS), allowing older adults of all types and their caregivers to address their needs at their preferred care location.

- Estimated cost: $250 million to $500 million from the MN state budget.

- A Medicare Companion Product

- Introduction of a new insurance product concept to address emerging care needs during retirement. This program would coordinate care across acute and LTSS needs through collaborative Medicare and LTSS supporting products.

- Two options proposed: a voluntary market-driven option or an obligatory option.

- The compulsory approach would provide $135 a day for one year, at an estimated cost of $120 a month at age 65.

- Premiums and benefits would increase by 3% annually.

- A Catastrophic-Lite State-Based Program

- Implementation of an obligatory state insurance program designed to assist with long-lasting, long-term care expenses for five years following a two-year elimination period. The focus is on home and community-based services (HCBS), with funds also available for facility care. Both employed and self-employed individuals would contribute to the program through payroll tax requirements.

- Benefits capped at a maximum of $50,000 per year, totaling $250,000 over 5 years, with annual 3% inflation.

- Estimated cost: 0.55% to 1.15% in payroll taxes.

New York

New York reintroduced Senate Bill 8462 on January 31, 2024, resembling the previous version but with several updates. Notably, self-employed individuals will now be subject to the tax. Additionally, four permanent exemptions have been included:

- Veterans of the U.S. military with a 70% or higher service-connected disability

- Individuals holding non-immigrant work visas

- Employees residing outside the state of New York

- Spouses or registered domestic partners of active-duty military personnel of the U.S. armed forces

Other enhancements from the previous version encompass pro-rata vesting for individuals born before January 1, 1972, who cannot meet the full 10-year lifetime vesting requirement. They will receive 1/10 of benefits for each year worked after the program's implementation. This updated bill also revises benefit qualifications from 3 out of 10 Activities of Daily Living (ADLs) to 2 ADLs, though without separate mention of cognitive impairment.

However, concerning any opt-out provisions, if offered, there have been no changes. New York's current definition of LTC insurance solely pertains to traditional LTC insurance, with hopes for an expanded definition encompassing a broader range of coverage.

Pennsylvania

Pennsylvania introduced a bill in 2022 and attempted again in 2023 without success. The bill primarily drew provisions from the WA Cares Fund "template," incorporating a premium tax of 0.58%. Although the bill included a tax exemption for LTC insurance owners, no further details were provided. It remains to be seen whether Pennsylvania will make another attempt in 2024 with the same bill or a revised version.

Summary

Long-term care and its effect on families have emerged as crucial and emotionally charged topics. Regrettably, publicly available articles often perpetuate numerous misconceptions regarding LTC insurance coverage. Contrary to outdated perceptions from 20 or 30 years ago, today's LTC coverage is more accessible to the middle class, features guaranteed premiums and benefits, and many policies are structured to safeguard the premiums paid if the policy is not utilized.

Deciding whether to opt out of a state mandated LTC program, if available, is an individual choice. Nonetheless, owning privately held LTC insurance—whether a state program is in place or not—and acquiring coverage sooner rather than later holds significant importance for several reasons:

- Choose the policy that suits your needs, providing benefits in the manner you prefer, including full cash indemnity benefits. State programs typically restrict payments to direct reimbursement to approved providers or offer reduced cash payments.

- Enjoy the assurance of guaranteed premiums and benefits. State LTC taxes might increase, or LTC benefits might decrease to maintain financial sustainability.

- Access greater benefit leverage, especially for high earners, as state programs may tax high-income earners more than the total available state LTC benefits.

- Have a wider array of care options. State programs often limit care choices to the state's approved providers list, requiring family caregivers to become state-certified and listed as approved care providers.

- Ensure guaranteed portability between states, as state programs may not allow benefits to be paid out of state (or country).

- Opt for guaranteed annual inflation protection, if desired, as state programs may not offer such guarantees.

- Secure premium protection with LTC products attached to life insurance (or annuities), as states do not refund unused benefits or premium taxes paid if benefits go unused.

- Seize the opportunity, as states have learned from past experiences to prevent a surge of opt-outs like in WA. Deadline dates may not be announced in advance. Planning ahead now saves on costs, improves inflation outcomes (if chosen), and establishes a policy before potential health declines.

- Enhance your marketability as a patient, as care providers and facilities prefer individuals with private insurance, often receiving billed rates. State programs may only reimburse care providers at Medicaid rates, which may not cover the cost of care.

*This information is intended to be educational and is not tailored to the investment needs of any specific investor. The information herein is general in nature and should not be considered legal or tax advice. Consult an attorney or tax professional regarding your specific situation.