As January 20, 2025, approaches, marking Donald Trump’s return to the White House, it’s time to prepare for potential changes to the U.S. tax code. The current tax framework largely stems from the 2017 Tax Cuts and Jobs Act (TCJA), which implemented significant reforms. However, many TCJA provisions include "sunset clauses" set to expire on December 31, 2025. Here's what to expect and how to plan.

Why Sunset Clauses?

U.S. tax laws consider federal budget impacts. To manage long-term deficits, Congress often sets expiration dates for tax cuts to limit their fiscal effect. This mechanism ensures tax legislation can pass without permanently increasing the federal deficit.

Three Scenarios Post-2025

- Full extension of TCJA provisions.

- Partial adjustments: some extensions, some changes, and some expirations.

- Complete repeal, reverting to pre-2017 tax laws.

With Trump’s return, the third scenario seems unlikely. Below, we examine key areas requiring attention.

- Individual Tax Rates and Deductions

Current individual tax rates (10%, 12%, 22%, 24%, 32%, 35%, and 37%) could increase by 1% to 4% per bracket if TCJA expires. Under Republican control, the current structure is likely to remain. Standard deduction levels are also expected to persist (e.g., $15,000 for single filers and $30,000 for joint filers in 2025).

- State and Local Tax (SALT) Deduction Caps

The $10,000 SALT deduction cap, contentious from its inception, has disproportionally affected taxpayers in high-tax states. Trump has proposed eliminating this cap, a significant shift from his original support for it. Adjustments to this provision remain uncertain, as bipartisan negotiations will likely shape its future.

- Child Tax Credit Adjustments

Both parties have proposed increasing the Child Tax Credit. At minimum, the existing $2,000 credit will likely be extended. Potential reforms include indexing the credit to inflation or modest increases, reflecting bipartisan interest in supporting families.

- Section 199A Deduction for Pass-Through Entities

The TCJA introduced the Section 199A deduction, allowing eligible business owners to deduct up to 20% of qualified business income (QBI). Restrictions apply to specific service businesses at higher income levels. Republican control suggests the deduction may persist or even expand, potentially increasing the deduction rate to 30%-35%.

- Estate Tax Exemptions and Strategic Planning

The Tax Cuts and Jobs Act (TCJA) significantly impacted estate tax planning for high-net-worth families by doubling the federal gift, estate, and generation-skipping transfer (GST) tax exemptions from $5.6 million to $11.2 million per individual. By 2025, these exemptions will increase further to $13.99 million per individual, allowing a couple with a combined net worth of $27.98 million to pass on their estate tax-free if they pass away within the year.

This temporary increase in exemption limits has led many affluent families to accelerate estate planning, leveraging the higher thresholds to transfer wealth out of taxable estates before the TCJA sunsets. While an extension of the elevated exemption amounts is possible under a Republican-controlled Congress, many families still find it prudent to transfer assets during their lifetime to mitigate potential tax exposure. The potential savings from pre-emptive planning could amount to millions in avoided estate taxes.

With the exemption likely to remain at TCJA levels, the urgency for immediate transfers has decreased for some. However, families should weigh the risk of transferring appreciating assets now versus retaining them in their estate to benefit from the step-up in basis at death, which could reduce capital gains tax liabilities for heirs.

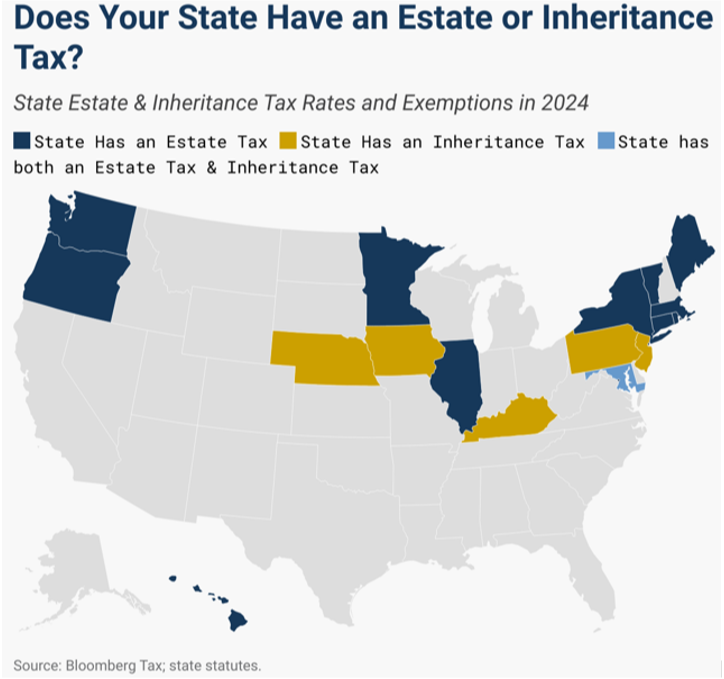

For estates already subject to estate taxes, transferring high-growth assets, such as rapidly appreciating business shares, into trusts can help exclude future growth from taxable estates. Additionally, residents of states with state-level estate taxes—such as Washington, Massachusetts, Oregon, and New York—may benefit from asset transfers to minimize state tax liabilities, even if federal estate taxes are not a concern.

Beyond tax considerations, trusts remain valuable tools for asset protection, ensuring wealth is distributed according to the grantor's wishes, shielding assets from creditors or divorce, and allowing individuals with disabilities to access public benefits without exceeding income or asset limits. Even without estate tax implications, these advantages make trusts an essential component of comprehensive estate planning.

- Emerging Tax Proposals

Trump’s campaign hinted at new policies, including exemptions for tips, overtime pay, and Social Security benefits. These ideas face significant implementation challenges due to potential fiscal impacts and system complexities. For instance, Social Security tax exemptions could cost up to $1.5 trillion, jeopardizing the program’s sustainability.

- The Political Realities of Extending the TCJA

In general, while the 2025 tax legislation is unlikely to significantly deviate from the scope of the original TCJA—given that the TCJA now serves as the baseline for much of the tax code—it is still poised to introduce notable changes across various areas of the tax system.

That said, one thing is almost certain: the “dream” of simplifying tax calculations and filing, as envisioned during the 2016 push for tax reform, remains far from realization. Any new tax cuts and corresponding offsetting tax increases included in upcoming legislation are all but guaranteed to add further complexity to the system.

Moreover, given that any extension or replacement of the TCJA may rely solely on Republican support, it is highly likely that the legislation will once again utilize the “reconciliation” process, enabling passage with a simple majority, much like the original TCJA in 2017.

This means that regardless of the form the new legislation takes, it will almost certainly include another sunset provision, with its expiration likely determined by the political landscape of the 2032 election.

As such, just as taxpayers—and the planners who advise them—conclude a seven-year period of speculation and preparation surrounding the TCJA’s sunset provisions, they will likely find themselves gearing up for yet another seven to eight years of planning for the next legislative cycle.

Once again, the key takeaway remains: early planning is essential!

Disclosure:

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. No strategy assures success or protects against loss. This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.